First home buyers squeezed + Brokers dominate lending + Refinancing jumps 20%

The first rung of the property ladder is getting higher, even for buyers targeting the lower end of the market.

Domain’s First Home Buyer Report for 2026 shows repayments on an entry-level house now absorb 48.9% of a young couple’s income across the capitals. That figure has climbed 24% in just five years. Units are less demanding, but still take 30.9% of income.

Saving the deposit is also taking longer. Nationally, it now takes five years to accumulate a 20% deposit for an entry-level house and three years and six months for a unit.

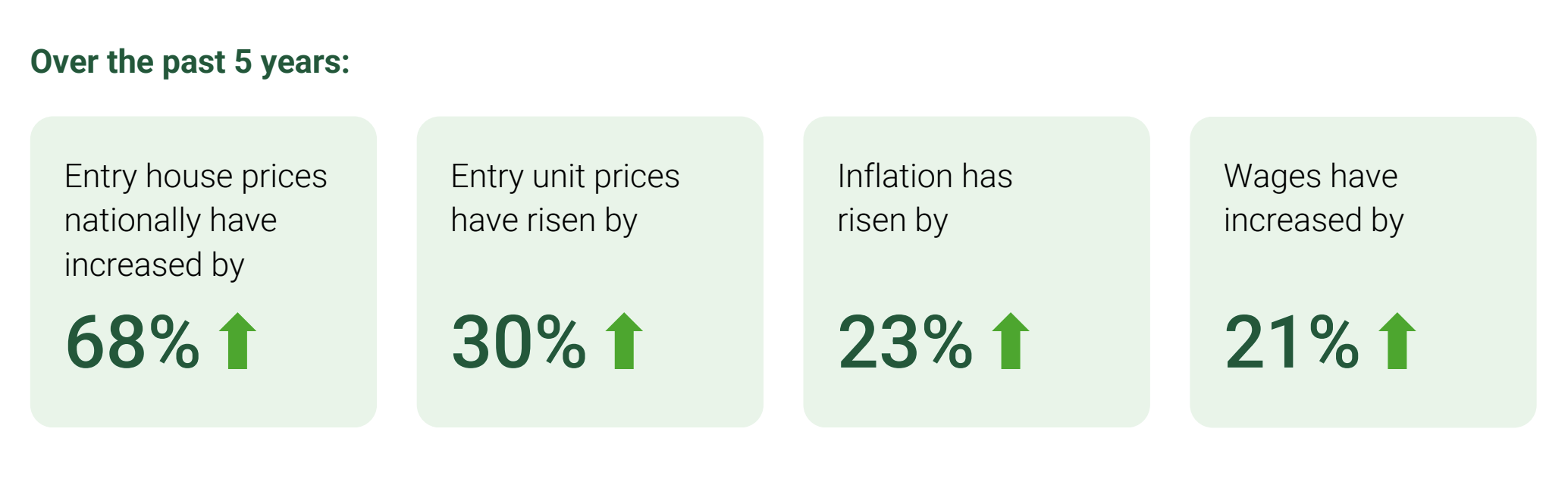

The shift becomes clearer when you compare property prices with wages. Over five years, wages rose 21%. Entry-level houses jumped 68% and units 30%.

At the same time, demand has continued to run ahead of supply. Limited new housing and tight listings have kept competition firm, particularly at the more affordable end.

Deposit support programs can help some buyers enter the market sooner. However, they do not reduce the share of income required to service a mortgage. And by bringing more buyers into the entry-level segment, they can also lift competition.

This doesn’t mean that homeownership is out of reach, but it does mean careful planning, realistic expectations and the right lending structure matter more than ever.

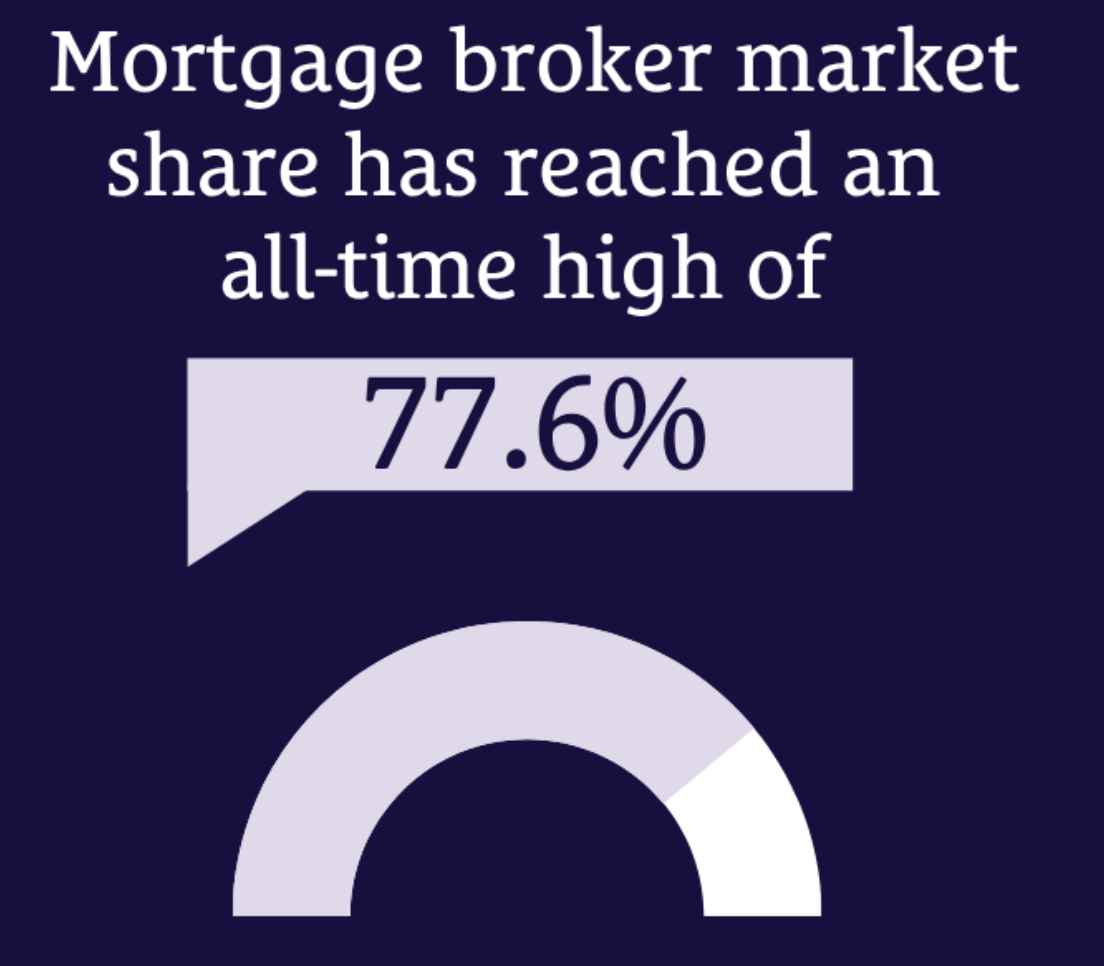

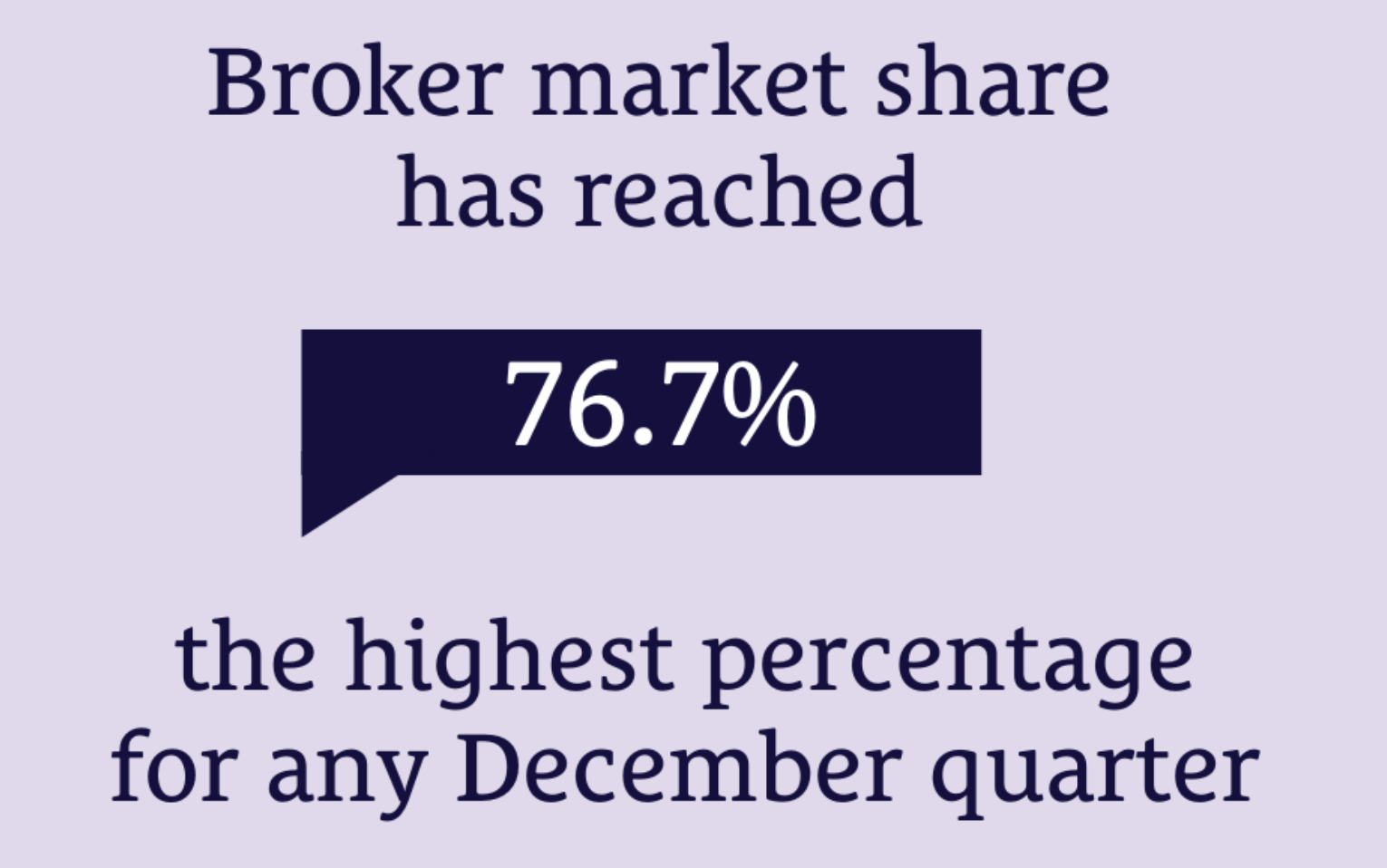

Brokers now write 76.7% of new home loans

More than three in four Australians are choosing a mortgage broker when taking out a home loan.

Brokers facilitated 76.7% of all new residential home loans in the December 2025 quarter, according to the Mortgage & Finance Association of Australia. That is the highest December quarter result since reporting began in 2013.

In dollar terms, brokers settled $142.20 billion in new loans during the quarter, up 9.2% on the previous quarter and 23.6% higher than a year earlier.

So why are brokers so popular?

Today’s lending market is complex. There are dozens of lenders, hundreds of products and constantly changing policies. A broker compares options across the market and helps borrowers find a loan that genuinely fits their circumstances, not just the headline rate.

That combination of choice, expertise and support is clearly resonating.

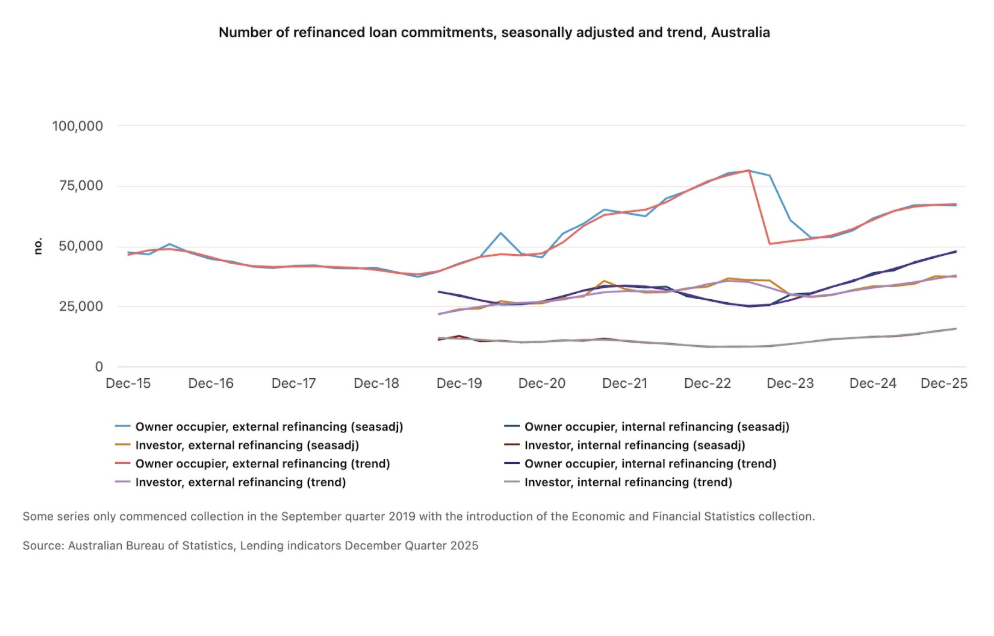

Refinancing surges 20% over the past year

More than 640,000 Australians refinanced their mortgage in 2025, according to the latest lending indicators from the Australian Bureau of Statistics.

That’s a 20% increase on the previous year.

As the graph below shows, after a dip in June 2024, refinancing activity has been steadily climbing in both value and number.

Interestingly, internal refinancing led the charge. The value of loans restructured with the same lender jumped 37% over the 2025 calendar year, while the number of those loans rose 26.8%.

That tells an important story. Borrowers are increasingly aware that loyalty does not automatically deliver a competitive rate. As a result, many are renegotiating with their existing lender, while others are moving entirely.

Strong refinancing growth reflects intense competition among lenders. However, making that competition work in your favour is not always straightforward.

This is where a broker can make the process easier. They can assess your borrowing position, compare options across the market and manage the transition if refinancing is worthwhile, helping ensure your loan remains competitive and suited to your circumstances.